Credit vs. Capital: Understanding the Financial Tools That Shape Your Borrowing Power

In today’s financial landscape, understanding the difference between credit and capital is crucial for both individuals and businesses. While the terms are often used interchangeably, they represent fundamentally different concepts that can greatly impact your financial decisions, borrowing power, and long-term financial health.

Defining Credit and Capital

Credit refers to the ability to borrow money with the promise of repaying it later, usually with interest. It is a tool that allows you to access funds beyond your immediate financial resources. Examples include credit cards, personal loans, mortgages, and lines of credit.

Capital, on the other hand, represents the financial resources you already own and can invest in your business or personal ventures. This includes savings, retained earnings, and equity investments. Capital is the foundation for building wealth and making strategic investments without relying on borrowing.

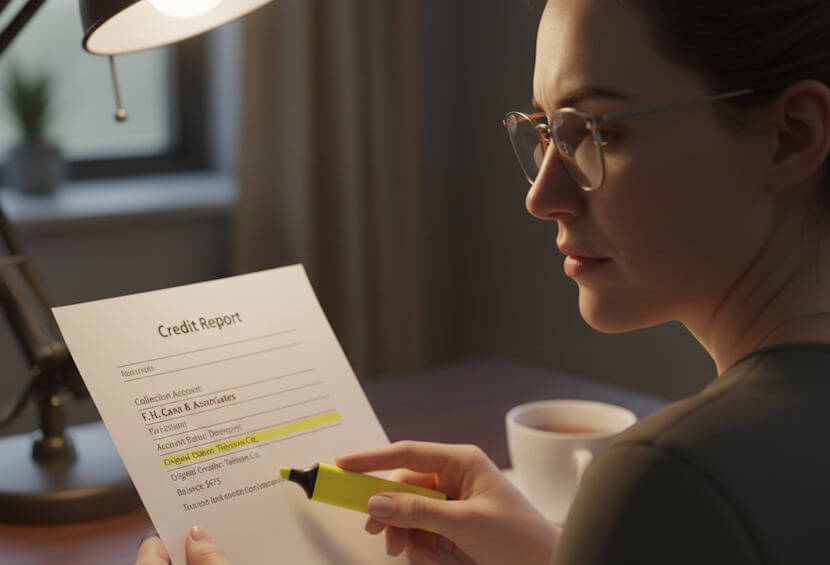

The Relationship Between Credit and Borrowing Power

Your borrowing power is significantly influenced by your creditworthiness, which is assessed by lenders based on your credit history, income, and existing financial obligations. For instance, accounts like F.H. Cann collection accounts can impact your credit score and, in turn, your ability to access favorable loan terms. Maintaining a good credit profile ensures lower interest rates and larger borrowing limits, making credit a powerful tool when used responsibly.

Advantages of Using Credit

- Liquidity: Credit allows access to funds when cash is tight.

- Flexibility: Credit lines and revolving credit offer flexibility in how and when you borrow.

- Building Credit History: Responsible credit usage improves your credit score over time.

Advantages of Using Capital

- Ownership: Using your own capital means you retain full ownership and control of your investments.

- No Interest Payments: Capital-based investments don’t require repayment or interest, reducing financial stress.

- Financial Stability: Investing capital demonstrates stability and reduces reliance on external financing.

Credit vs. Capital: Key Differences at a Glance

| Aspect | Credit | Capital |

|---|---|---|

| Definition | Borrowed funds to be repaid with interest | Funds you own and can invest |

| Source | Lenders, banks, financial institutions | Personal savings, retained earnings, equity investments |

| Risk | High if mismanaged (debt, penalties, damaged credit score) | Lower, though investment losses are possible |

| Impact on Borrowing Power | Directly affects your ability to borrow more | Indirectly affects borrowing through asset strength and collateral |

When to Use Credit vs. Capital

Deciding whether to use credit or capital depends on your goals, financial situation, and risk tolerance. Here are some general guidelines:

Use Credit When:

- Cash flow is temporarily tight but future income is expected to cover repayment.

- There’s an opportunity that requires immediate funding.

- You want to build or improve your credit history responsibly.

Use Capital When:

- You want to maintain full control and avoid debt obligations.

- Long-term investment potential outweighs immediate borrowing benefits.

- You have sufficient funds to cover your investment without jeopardizing liquidity.

Strategies for Balancing Credit and Capital

Successful financial management often involves a strategic balance of credit and capital. Here are some practical strategies:

- Leverage Credit Wisely: Use credit for high-return opportunities but avoid overextending yourself.

- Maintain Adequate Capital Reserves: Keep savings and liquid assets to reduce dependence on borrowed funds.

- Monitor Credit Reports Regularly: Ensuring accounts are accurate helps protect your credit score.

- Evaluate ROI: Always compare the cost of credit versus the opportunity cost of using your capital.

Common Pitfalls and How to Avoid Them

While both credit and capital are valuable financial tools, misuse can lead to significant challenges:

- Overleveraging: Borrowing too much without adequate repayment capacity can lead to debt traps.

- Underutilizing Capital: Holding too much cash may reduce investment returns.

- Ignoring Credit Health: Neglecting your credit profile can limit future borrowing options.

Practical Example: Funding a Small Business

Imagine you are starting a small business. You have $50,000 in personal savings (capital) but require $100,000 to cover initial costs. You might:

- Invest $50,000 of your own capital to retain ownership.

- Secure a business loan or line of credit for the remaining $50,000 to bridge the gap.

This approach allows you to leverage both resources strategically, optimizing your borrowing power while minimizing risk.

Long-Term Benefits of Understanding Credit and Capital

Mastering the distinction between credit and capital empowers you to:

- Make informed borrowing decisions.

- Maximize investment returns.

- Build financial resilience in both personal and business finances.

- Protect and enhance your creditworthiness over time.